In 1899, George Wingfield was a nineteen-year-old cowboy when he attempted to borrow money collateralized by his last worldly possession, a woman’s diamond ring.

In 1899, George Wingfield was a nineteen-year-old cowboy when he attempted to borrow money collateralized by his last worldly possession, a woman’s diamond ring.

The banker initially thought George to be “something of a shambler*.” However, after asking him what he intended to use the money for, he became convinced that there was something special about Wingfield, “the kind of square Western gambler that even a Nevada banker could rely upon.” He loaned him a nominal amount of money; the exact amount is lost to history, but is generally agreed to be between $25 and $75. The loan was quickly repaid, and the banker agreed to provide Wingfield with a $1,000 grubstake, in exchange for fifty percent of the future wealth created by the cowboy’s efforts.

Within five years of their initial meeting, Wingfield had leveraged his modest grubstake into a mining enterprise worth in excess of $50 million, making the former cowboy and his banker two of the richest men in the Western United States.

The factors that led the banker to grant Wingfield his grubstake are the similar to those which drive modern-day, high-tech venture capital investments.

What is a grubstake and how did Wingfield convince the banker to grant one to him? Read on.

If you haven't already subscribed yet, subscribe now for

free weekly Infochachkie articles!

“Grubstake” is a very American word, combining “grub” meaning “food” with “stake” meaning “a share or interest in a commercial enterprise.” Merriam-Webster defines Grubstake as: “Supplies or funds furnished a mining prospector on promise of a share in his discoveries; material assistance (as a loan) provided for launching an enterprise or for a person in difficult circumstances.”

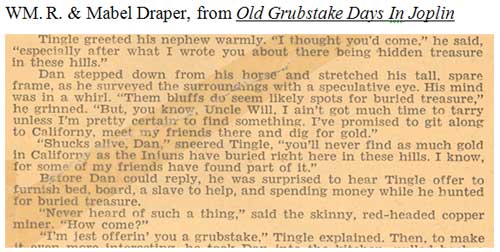

As described in the excerpt from Old Grubstake Days In Joplin above, a grubstake often involved the financier or Grubstaker funding the entrepreneur’s or Grubstakee’s food, lodging and tools required to execute the adVenture.

Wingfield’s fortune was not the only one derived from a small grubstake. Old Grubstake Days In Joplin goes on to describe how Dan’s tireless labor and his keen eye for geological anomalies, combined with his uncle’s financial wherewithal, resulted in the discovery of the fourth-largest U.S. lead mine and the most productive zinc mine of its era.

The Less Things Change, The More They Stay The Same

Although it is tempting to over-intellectualize modern-day venture capital, when boiled down to its essential elements, it differs only slightly from the Grubstaking which took place in the Western United States during the latter portion of the 1800s. Contemporary venture capitalists do not typically provide an entrepreneur room and board, but they do often establish salaries based on an entrepreneur’s nominal living expenses. In this way, the majority of a startup’s funds can be applied directly to further the adVenture’s success, rather than to make life comfortable for the entrepreneur.

Grubstakers sought Grubstakees with the traits described in Youthful Discretion – usually a young person with passion, hunger and sufficient skills to autonomously pursue the adVenture. Frontier financiers put credence in the same characteristics that are valued by contemporary venture capitalists, including:

Informal Education – Consideration of a Grubstakee’s formal education was usually irrelevant. If the Grubstakee had any “book learning,” it was seldom directly applicable to the nature of the grubstaked adVenture. A Grubstaker focused on proof of an individual’s ability to perform the skills required to succeed at the proposed enterprise, not his ability to prosper in otherwise esoteric environments, such as a classroom.

Stewardship – Judicious use of funds was of the utmost importance, because the Grubstaker was directly footing the Grubstakee’s bills. As such, the miserly spending approach described in Frugal Is As Frugal Does was a prized Grubstakee trait.

Clean Backtrail – Without email, Twitter or an iPhone, Grubstakers verified a Grubstakee’s propensity toward honesty, integrity and hard work by asking a few well-placed questions to the folks who had previously crossed paths with the Grubstakee.

No B.S. – A firm handshake, coupled with direct eye contact, was often the only contract underlying a Grubstake deal. As such, communications had to be clear, open and direct. If a Grubstaker asked, “Where do you intend to mine for gold?”, a response of, “That is confidential information, but I will consider sharing it with you once you sign my NDA,” would not result in a Grubstakee receiving subsidized room and board.

Sticktoitness – Most men who accepted a grubstake felt honor-bound to repay them, even if the funded adVenture never generated a profit. Grubstakers funded Grubstakees who demonstrated a Humble Pride and considered failure a personal affront.

Shared View Of Success – The Grubstaker won when the Grubstakee won. Such alignment minimized the risk that Founderitis would arise and derail the adVenture. A Grubstakee who attempted to withhold profits rightfully earned by a Grubstaker usually met his demise face-down on a barroom floor, as opposed to in a courtroom.

Fear Of Failure – A grubstake was intended to facilitate the Grubstakee’s basic survival while he pursued his adVenture, not satiate his hunger for success. If the grubstake was too large and the Grubstakee was not properly motivated, the adVenture would fail. Effective Grubstakees were sufficiently dissatisfied with the lifestyle afforded by the grubstake and did not consider free room and board “success,” just as veteran, modern-day entrepreneurs do not consider a funding event a “victory.”

Fill The Scarcity Void

“I don’t ask for much, I only want your trust.

But you know, it don’t come easy.”

Ringo Starr and George Harrison, It Don’t Come Easy

As noted in Spilling The Beans, ideas are innumerable, and in the absence of competent execution, they are worthless. Conversely, money in pursuit of outsized returns is plentiful. Thus, if both ideas and money are abundant, what is the scarce constraint in the entrepreneur/venture capital fundraising equation?

The scarce commodity is trust. Trust brings ideas and money together. As such, an entrepreneur’s task is to create a bridge of trust between his ideas and the venture capitalist’s cash.

Trust is what brought together George Wingfield’s energy, drive, ambition and ideas with his banker’s grubstake funds. Wingfield went on to become known as “King George,” due to his political influence, which was so pervasive that he turned down an appointment to the U.S. Senate because he feared that relocation to Washington, DC, would dilute his power.

King George was also known for his generosity and willingness to grubstake miners and ranchers whose earnest work ethic and Creed were sufficient to earn his trust. This approach allowed King George to reap the rewards of numerous entrepreneurs’ hard work, without getting his hands dirty – just like a modern-day venture capitalist.

______________________

John Greathouse has held a number of senior executive positions with successful startups during the past fifteen years, spearheading transactions which generated more than $350 million of shareholder value, including an IPO and a multi-hundred-million-dollar acquisition.

John is a CPA and holds an M.B.A. from the Wharton School. He is a member of the University of California at Santa Barbara’s Faculty where he teaches several entrepreneurial courses. He is also the author of an award-winning entrepreneurial blog infoChachkie.com. You can learn more about his experiences at johngreathouse.com

______________________

<

Copyright © 2007-9 by J. Meredith Publishing. All rights reserved.

-----

George Wingfield: Owner and Operator of Nevada <Return to Article>