Randy Churchill and his team at PricewaterhouseCoopers meticulously prepare a quarterly report detailing the venture landscape, called Shaking The Money Tree. The data consistently confirms that: (i) venture capitalists are typically not adventuresome, and (ii) most startups lack the three intoxicating factors which cause venture capitalists to pull out their checkbooks.

Randy Churchill and his team at PricewaterhouseCoopers meticulously prepare a quarterly report detailing the venture landscape, called Shaking The Money Tree. The data consistently confirms that: (i) venture capitalists are typically not adventuresome, and (ii) most startups lack the three intoxicating factors which cause venture capitalists to pull out their checkbooks.

If you haven't already subscribed yet, subscribe now for free weekly Infochachkie articles!

The Three Enthralling Factors Of Venture Funding

Naval Ravikant, Co-Founder of AngelList and Venture Hacks, details a variety of factors that influence your chances of raising venture funding in this informative interview. Of the factors referenced by Naval, three which are difficult to directly influence have a disproportional impact on an entrepreneur’s ability to secure institutional funding: location, sector and stage.

I do not advocate that you perform unnatural acts in an attempt to make your company more advantageous to venture funding. However, it is prudent to be acutely aware of these factors as you engage in your fundraising efforts.

LOCATION: I Wish They All Could Be California Companies

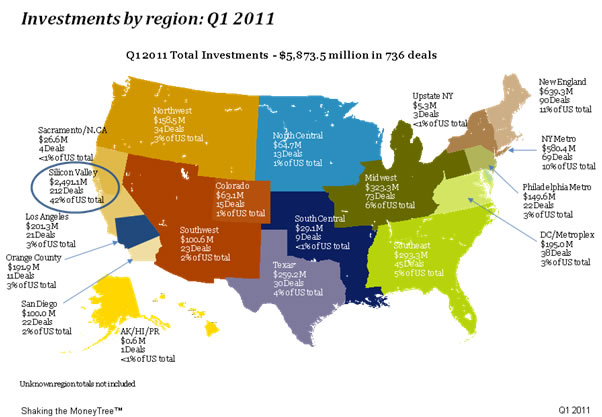

A clear trend over the past 15-years is that many Silicon Valley venture capitalists enjoy investing within driving distance. As an early stage investor, I recognize the importance of being accessible to your portfolio executives, so a concentration of venture funding in Silicon Valley is certainly not a surprise. However, the fact that nearly half of all venture funding in the United States consistently occurs in Silicon Valley is shocking.

This concentration is partly due to natural causes – successful startups spawn other successful startups. It is also somewhat of a self-fulfilling prophecy. If the tech community believes that a certain area is the epicenter of a particular industry, motivated entrepreneurs will start their ventures in such locations, thus reinforcing the geography’s perceived advantageousness. A more nefarious reason for the density of Silicon Valley startups is the fact that many of the venture capitalists make relocation to their backyard a condition of funding.

Partners at large venture firms generally believe that Orange County is the ideal geography for medical devices, San Diego for telecom and life sciences (along with Boston) and Silicon Valley for everything else. Other than shortening the investor’s quarterly commute to your Board meetings, the net benefits of relocating for many startups are illusory, as I describe HERE. For years, well-intentioned venture capitalists asked me when we planned to move Computer Motion (NASDQ: RBOT, sold to Intuitive Surgical) and Expertcity, (creator of GoToMyPC and GoToMeeting, sold to Citrix). Despite the fact that we never moved, both companies were successful.

I recently spoke with an unhappy early-stage investor who described the demise of a life sciences startup which was moved from Santa Barbara to San Diego at the behest of a large venture firm. The Partner at the big firm was convinced that it was impossible to grow a medical company in a backwater town. I guess no one told him about the medical startups that were purchased by Medtronic, Linvatec, Storz, Mentor, etc., all of which continue to thrive in Santa Barbara to this day.

The uprooted company found that less of their time was spent developing valuable science and more was devoted to finding (more) expensive office space, negotiating with (more) expensive employees all the while fighting to retain transplanted employees who hated San Diego. End result, the company’s product timeline has been pushed back substantially and the company’s morale is at an all-time low. Thanks Mr. Big Firm VC.

Naval Ravikant describes how Silicon Valley’s dominance over the venture capital landscape will evolve over time in the previously mentioned interview.

STAGE: Few Harvests, Little Planting

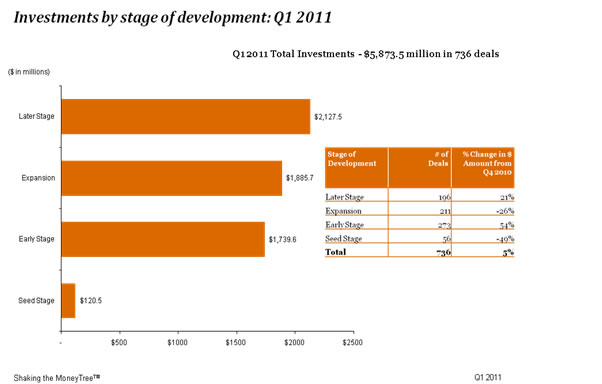

As shown in the following chart, the overwhelming focus of investments during Q1 of 2011 was in later stage companies. This is not a quarterly anomaly – this trend has held firm for over a decade.

The lack of exits in the last few years has certainly impacted this statistic, as venture capitalists have been forced to continue investing in some portfolio companies beyond their expected exits. However, a review of historical data confirms that this trend remains consistent, even in boom times.

SECTOR: Software, Energy, Bio Or Bust

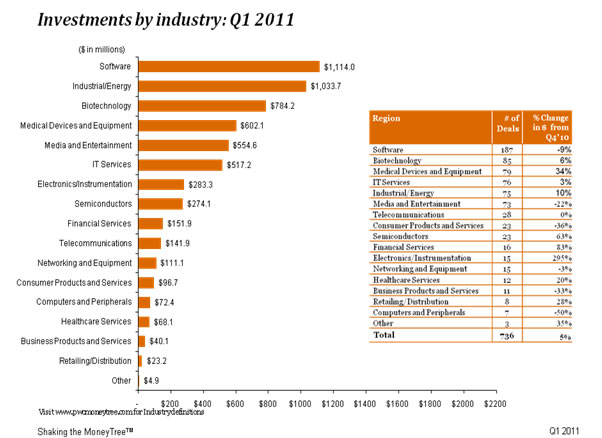

In addition to the geographic and stage concentrations prevalent among venture funded businesses, venture capitalists also focus most of their attention on a handful of industries. Notably, there were 426 investments made in software, medical and clean tech energy companies during Q1 2011, which represents 58% of all the tracked deals and 60% of the total dollars deployed. Although clean tech is a relatively recent sector, historical concentrations in software and healthcare date back to the early 1980s.

Do The Math

Consider your adVenture’s stage, geographic location and sector when assessing the likelihood you will obtain venture funding. For instance, if you run a later-stage software company located in Silicon Valley, then your prospects of obtaining future venture financing are highly favorable. However, if you operate an early-stage financial services company headquartered in the Southwest, consider the following:

Southwest percent of total VC money deployed = 2%

Financial Services percent of total deals = 2.58%

Early stage percentage of total deals = 2.05%

Although the math is imperfect, it is instructive to calculate the relatively small dollars that are likely to be applied to this particular venture by multiplying the total VC dollars deployed in Q1 2011 by the above percentages. The resulting $62,000 is theoretically available to early stage, financial services ventures based in the southwest. The reality is that such funding events are binary, they either happen or they do not. Even so, the above analysis illustrates how unlikely it is for an. The Founders of such a startup would be well served to invest their time pursuing non-venture capital funding.

Nine Positions I Do Not Need

The fact that something is difficult or even unlikely will not deter a determined entrepreneur. At one time in my career, I was told, “The chances of you getting accepted are low, as there are only ten positions.” I laughed and said, “Great, that is nine more than I need.”

Savvy entrepreneurs understand that venture capitalists are just one of many sources of funds. By better understanding the three intoxicating factors which predominantly influence VCs, entrepreneurs can efficiently focus their fundraising efforts on the most likely sources of capital.