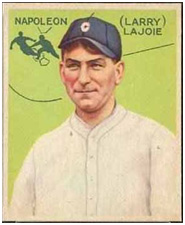

In 1933, baseball card collectors were frustrated. For some reason, they found it impossible to complete their Goudy Gum 240-card set. No matter how many packages of cards they purchased, they failed to find card number #106, which featured Napoleon Lajoie.

In 1933, baseball card collectors were frustrated. For some reason, they found it impossible to complete their Goudy Gum 240-card set. No matter how many packages of cards they purchased, they failed to find card number #106, which featured Napoleon Lajoie.

Enterprising collectors who wrote Goudy and voiced their frustrations were rewarded by receiving the Lajoie card in the mail. All other collectors were out of luck.

What was behind the mystery of the missing Lajoie card?

If you haven't already subscribed yet, subscribe now for

free weekly Infochachkie articles!

Capital Cards

In 1976, at the age of 14, I Co-Founded a Sports Memorabilia company with my friend (and future brother-in-law). We pooled our resources and each invested $50 into the adVenture, which we named Capital Cards, due to our proximity to Washington, DC. Over the next six years, we grew the company into a thriving mail-order business, with assets conservatively estimated at approximately $250,000. Not a multimillion dollar exit by any means, but a fantastic learning experience and a lot of fun as well.

Our strategy was simple. Each week, we placed a small classified ad in the Washington Post, simply stating, “Turn your cards into cash. We will purchase your old baseball cards.” During the mid-1970’s, the sports memorabilia industry was nascent and highly inefficient. It was a great time to start a sports memorabilia company. The hobby was driven principally by collectors who were primarily interested in completing sets. There were very few card dealers and no card investors. There were no price guides, standardized rating systems or baseball card stores. People with vintage cards essentially had no means to convert their cards into cash.

We quickly built upon our meager initial capital by buying and selling cards that otherwise would likely have ended up in landfills. Each weekend, we drove all over the Washington beltway in search of lost treasures. In many cases, we came across cards which we had never seen and had no way to estimate their value. This ambiguity put us on a level playing field with the card sellers.

We were also one of the first card companies to purchase cases of cards directly from Topps, the only company that produced sports cards at that time. Our parents had to sign on our behalf, as we were not of legal age to execute purchase orders.

Each case contained 12,000 randomly sorted cards. We enlisted the help of our families and friends and arranged the cards into complete sets. We then sold the sets at card shows held in small towns all along the East Coast. At each show, we were far and away the youngest participants. Fortunately, my brother-in-law was old enough to drive, so we were able to attend the shows without our parents’ involvement.

Because our labor was essentially free, we undersold all the other dealers at the shows. In fact, in one instance, a dealer purchased all of our sets in order to “take them off the market.” We were happy to accommodate his request, as the money derived from the sale of the sets allowed us to purchase vintage cards via our weekly newspaper ads.

As noted in Small Ideas, Big Benefits, Capital Cards was an exceptional experience for both me and my brother-in-law, as it allowed us to hone our business skills, while competing with people who were more than twice our age.

At heart, we were idealistic and somewhat sanctimonious collectors. We loved sports and valued the cards because of the players’ achievements. Card collectors and card investors have very different motivations. Card investors seek cards which they believe will increase in value and are often indifferent regarding the players and teams depicted on the cards. My Partner and I eventually closed down Capital Cards when baseball card collecting morphed from a hobby into an investor-driven industry.

But Our Hobby Is Different…

During the early 1980’s, the popular press discovered baseball card collecting and began to publish articles touting sports memorabilia as a great “investment”. Many baseball card collectors believed that the sports memorabilia hobby would not follow the evolutionary path of other hobbies which became investor centric, such as stamp and coin collecting.

However, as the number of non-collectors entering the sports memorabilia market in pursuit of financial gain increased, the dynamic of the industry changed and evolved in a manner similar to other mature collectible markets.

For instance, the range between what a collector could sell a card for versus what they had to pay for the same card from a dealer diverged significantly. In addition, rigid grading systems were established by professional grading services. This dramatically increased the value of the highest graded cards and depressed the prices of all other cards which did not meet the exacting standards of the grading services.

In the early days of collecting, the various grades, Mint, Excellent, Very Good, Good and Poor, were highly subjective. As such, the relative difference in value between a Mint and an Excellent card was not significant. Many collectors, whose primary goal was to complete their collections, were content to have an Excellent or even a Very Good card, which ensured broader demand for lesser grade cards. The advent of investors and grading services drove up the demand for near-perfect cards while suppressing the value of all other cards.

As the industry matured, several new companies began competing with Topps by producing their own sports cards. In the collector days, Topps would generally issue a single set of cards each year. As the collector centric hobby morphed into an investor-driven market, several card companies began producing multiple sets annually. This resulted in a saturation of new cards which eventually suppressed the value of all non-vintage cards.

Eventually, card buying speculation drove prices ever higher. A prime example is rookie cards, which were priced like Initial Public Offering shares of stock. Investors were willing to pay a premium for a card of an unproven rookie in the hopes that his future performance would cause the price of the card to increase over time. Conversely, collectors tended to value the cards of proven, Hall of Fame players.

No Really, Our Industry Is Different…

Card collectors were in denial during the late-1970’s. Even as we saw our hobby began to change, we believed it would never become an investor oriented industry. Over time, our belief dissolved into hope, which eventually became dismay. Despite our desires, the sports memorabilia hobby changed in the same, predictable manner as other popular hobbies.

It is not uncommon for the pioneers who drive emerging industries to believe that their industry will not follow the “rules of the road” of related more, mature industries. Gary Kildall, who refused to Conform To His Customers’ Realities, felt that the parameters of the personal computer industry would be defined by the passionate PC hobbyists who drove its early development. He failed to realize that the industry would eventually attract mainframe and minicomputer industry veterans who would bring market strategies and doctrines based on the legacy industry’s orthodoxy.

In the early days of the Internet, the ad market seemed to be completely different from any media which had preceded it, primarily due to the unprecedented ability for advertisers to track the effectiveness of their campaigns, as discussed more fully in Managing Your Cost Per Customer. However, as the Internet advertising industry matured, it became populated with traditional media veterans who infused old-world jargon (e.g., Insertion Orders, Trafficking, Flight Dates, etc.) as well as old-world pricing, such as cost-per-thousand views, which was based upon print advertising metrics. Eventually the industry matured and hybrid pricing schemes were developed, such as cost per action, cost per click, etc. However, the fundamental tenets of the online ad industry are akin to those established in the pre-Internet world.

Hoping your industry does not change is unrealistic. Instead, anticipate how your emergent industry will mature by analyzing the structure of adjacent and legacy markets. As your industry grows, it will attract refugees from these related markets, who collectively will strongly influence your industry’s transformation. The challenge is to anticipate which innovative aspects of your industry will survive this inevitable maturation.

The Joy Of Lajoie

Napoleon Lajoie’s scarcity was the result of Goudy Gum intentionally not including the card in retail gum packs. They knew that collectors are driven by the desire to complete sets and that a missing card would cause them to purchase additional packs. Ironically, in the modern, investor-driven baseball card industry, Lajoie’s card is prized not because it is key to completing the Goudy Gum set, but because of its propensity to appreciate. Few modern-day card investors attempt to complete a Goudy Gum set, but all of them long for the rare Lajoie card, as its scarcity ensures it is an investment that will increase in value over time.

______________________

John Greathouse has held a number of senior executive positions with successful startups during the past fifteen years, spearheading transactions which generated more than $350 million of shareholder value, including an IPO and a multi-hundred-million-dollar acquisition.

John is a CPA and holds an M.B.A. from the Wharton School. He is a member of the University of California at Santa Barbara’s Faculty where he teaches several entrepreneurial courses.

______________________

<

Copyright © 2007-10 by J. Meredith Publishing. All rights reserved.